The Sayrafa electronic exchange platform is the primary means by which Banque du Liban (BDL), Lebanon’s central bank, intervenes in the country’s currency market.

When the Lebanese lira is in trouble and collapsing in value, Sayrafa is how the BDL swoops in to save the day, injecting the market with United States dollars to steady the exchange rate and save the population from further inflation and hardship.

That’s the story the bank would have you to believe anyway – and given that the central bank has kept us almost completely in the dark about how the platform is being used, it can be hard to prove wrong.

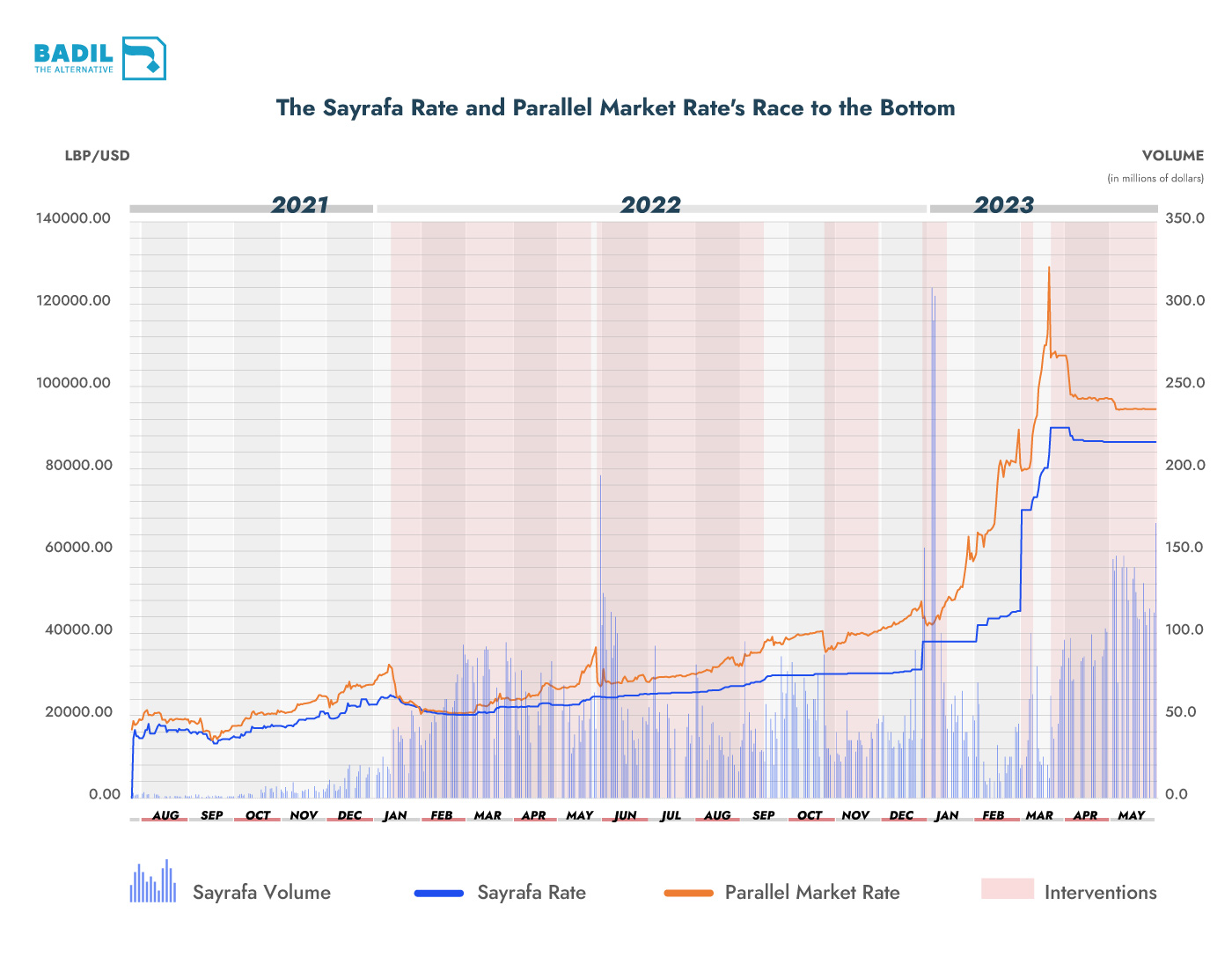

The indicators that are available, however, point to a very different story. Since the beginning of 2022, the BDL has announced six interventions in the currency market using Sayrafa, with all but the most recent, in March 2023, having limited impacts on the market exchange rate.

In reality, the largest function of Sayrafa appears to be to act as a subsidy for banks, importers, businesses and the wealthy, by selling them US dollars at a substantial premium relative to the parallel market exchange rate and then allowing them to profit from arbitrage. This appears to constitute most of the money traded on the platform.

As the value of the lira has collapsed since 2019 and the value of local salaries with it, the patronage networks the political elite have sustained through the public sector have been unraveling. The BDL allowing civil servants to withdraw their salaries in dollars exchanged at the Sayrafa rate thus also acts as a subsidy for these workers. While the amounts traded for this purpose on the platform are fractional relative to the volume of large-scale money trades, they offer a degree of relief for public service employees that has likely quelled even greater unrest than the country is already experiencing, thereby helping the political elite to maintain some relevance among their constituencies.

In the following explainer, The Alternative examines the BDL’s much-touted Sayrafa platform and deconstructs the hype.

How BDL sinks, then stabilizes, the lira

During April and May, the parallel USD/LL rate plateaued between 97,000 and 94,000, marking what on the surface appears to be a successful move by the Banque du Liban (BDL) to wrestle the volatile lira under control. This period of relative calm came after the central bank announced it would begin selling an unlimited number of fresh dollars to prop up the lira after a sharp drop in its value in March, when the price of a dollar touched 141,000 LL.

The central bank has injected dollars into the Lebanese economy in the same manner five times since the beginning of 2022, although previous interventions saw comparatively less success than the most recent. The Sayrafa should thus be considered a “weak and inefficient monetary tool”, as the World Bank noted in a recent report, with only a low overall correlation between interventions and the exchange rate.