One year has passed since the Beirut Port explosion of August 4, 2020. As summer temperatures are hitting record highs, so is the political temperature in Lebanon. The families of explosion victims have endured 12 months of lack of accountability and blatant interference in the judicial process. Public anger is simmering and threatening to boil over into another wave of unrest.

As the painful anniversary was drawing nearer, the European Union announced a framework that “provides for the possibility of imposing sanctions against persons and entities who are responsible for undermining democracy or the rule of law in Lebanon”. The long-anticipated move is effectively a warning shot aimed at pressuring Lebanon’s intransigent elites into undertaking reforms.

Those same elites who presided over the explosion have shirked responsibility for Lebanon’s spiralling economic crisis – assessed by the World Bank as among the worst ever recorded. Political leaders have prioritised partisan squabbles over rebuilding the country, failing to replace the government that resigned after the explosion.

While pressure from the West is welcome, targeted sanctions on Lebanon’s politicians risk missing the mark unless they are more effective in their attack on the actual power structure of the country. And in Lebanon, true power – and culpability – lies in the nation’s banking sector, which is responsible for the ongoing economic demise of the country.

Together with the Banque du Liban (BDL), Lebanon’s central bank, commercial banks engaged in a regulated national Ponzi scheme that dug an $80bn public debt hole in the country’s finances. Instead of instituting capital controls and enacting a recovery plan, the BDL and the banking sector devised their own shadow financial plan, which employed blatantly illegal multiple exchange rates, informal capital controls, and the printing of vast amounts of local currency.

This current arrangement, which would surely qualify as misconduct under the EU sanctions framework, shunts the crushing burden of the crisis onto ordinary Lebanese, who have to take an up to 80-percent cut on their cash withdrawals.

These non-solutions have obliterated the life savings of the Lebanese people and left them struggling with chronic shortages of electricity, food, and pharmaceuticals – the import of which the BDL can no longer afford to subsidise from the country’s fast-dwindling foreign currency reserves. Yet, those with sufficient connections to the banking sector have already moved their money offshore, with an estimated $30bn leaving the country since mid-2019.

Sanctioning the banking sector would offer Western policymakers a technically sound and more effective regime than the “framework” proposed by the EU. That is because, to function effectively, sanctions need to be directed at a clearly defined group of individuals and entities that are culpable, have the power to influence change, and feel threatened by sanctions.

At present, the proposed EU sanctions target Lebanon’s political leaders, many of whom do not necessarily meet those criteria or who have demonstrated that they are unwilling to challenge the BDL or the banking sector, not least because of current or previous business ties to the industry.

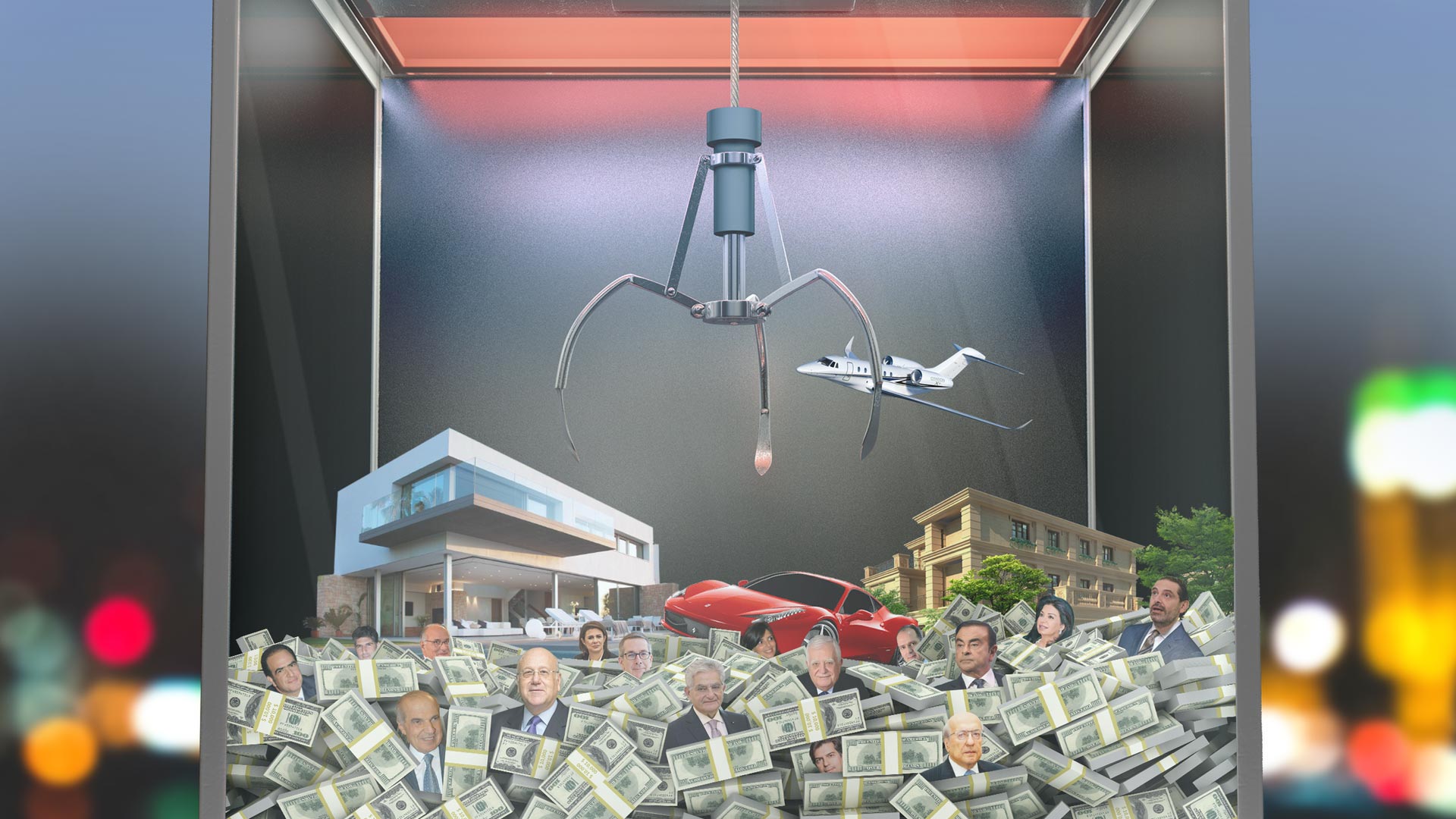

A seminal study from 2016 found that individuals closely linked to the political elite controlled 43 percent of assets in Lebanon’s commercial banking sector. The same research found that eight families controlled 29 percent of the banking sector’s assets, led by the family of former Prime Minister Saad Hariri.

Through the investment company GroupMed Holding, the Hariri family currently controls the majority stake in BankMed, one of the largest banks in Lebanon. Saad Hariri’s successor as premier-designate, fellow billionaire Najib Mikati, who was under investigation for embezzling a state-backed housing fund, has close ties to Bank Audi, Lebanon’s largest bank by assets. Mikati’s brother and business associate, Taha, has a stake in Bank Audi through his investment company, Investment & Business Holding.

Both Hariri and Mikati have had ample chances to reform the banking sector and public finances when they were premiers. They did not do so and there is no reason to think they will do it in the future.

That is why direct sanctions on financial leaders might be more effective. For example, sanctions on BDL officials could help Lebanon strike a fair bailout deal with the International Monetary Fund. Currently, the main stumbling block before securing a loan programme is the need for an audit of the BDL. In the past, the central bank has repeatedly obstructed this process and would continue to do so until the current BDL governor and commercial banks have a real incentive to facilitate it – something which targeted EU sanctions could provide.

Smarter sanctions against Lebanese banks and bankers would also compel foreign institutions and businesses to stay away from Lebanon’s tainted banks. Years of soaring, irresponsible interest rates have attracted all sorts of hungry investors, including Arabian Gulf royals, the European Bank for Reconstruction and Development (EBRD), the World Bank-affiliated International Finance Corporation (IFC), and France’s official development agency, Agence Française de Développement (AFD).

At least for Western institutions, retaining stakes in banks directly involved in the “deliberate” economic meltdown of an entire nation should be an obvious moral hazard. The threat of Western sanctions would surely encourage them to pull out of Lebanon’s banking system.

While sanctions as an international pressure tool have sometimes been criticised for resulting in unfair collective punishment of whole nations, fears that the Lebanese people would suffer from such measures imposed on their financial leaders are also unfounded. It is hard to conceive how sanctioning the banks that devour people’s deposits could worsen the situation. If the sanctions are targeting specific individuals within the country’s financial elite, this would prevent any spillover that could affect the Lebanese public.

Furthermore, sanctions on the Lebanese financial sector have already proven effective in immediately producing change in the country. Over the past decade, two Lebanese banks were brought down by a simple edict from the US Department of the Treasury over suspected money laundering for Hezbollah.

Pressure from the US also cracked open Lebanon’s antiquated banking secrecy regime for the first time, as Lebanese banks sought to comply with Washington’s Foreign Account Tax Compliance Act. The law requires banking institutions to provide information to US tax investigators about American customers.

Without decisive action, the future looks incredibly bleak for Lebanon, which is fast becoming a failed state. Should that happen, a repeat of the 2015 migrant crisis is not inconceivable; neither is another wave of radicalisation akin to the one which spawned ISIS.

Instead of watching on the sidelines as another political and humanitarian crisis unravels, the West could impose sanctions on the financial sector to turn the tide of Lebanon’s collapse. And the only cost of such measures would be making some already well-off bankers and politicians just a little less rich.

This commentary was originally published in Al Jazeera.